BANC ONE CORPORATION

An Analysis of their Hedging Strategy

By

Mark Glitto, Gajendra Tulsian,

Robert Young

University of

Florida

Summer 1997

INTRODUCTION

In 1993 the stock price of Banc One Corporation had dropped from about $45 at the beginning of the year to approximately $35 at the end of the year: roughly a 20% fall. This sharp decline in stock price greatly bothered John B. McCoy, chairman and CEO of Banc One Corporation. A high stock price was essential for Bank One’s strategic goal of continued acquisition by tendering its own stocks in each acquisition. The fall in stock prices put a damper on this drive for acquiring banks with potential for earnings and growth (it had 10 pending acquisitions worth $9 billion in November 1993). In this study we analyze the possible reasons for the fall in stock price and suggest ways to stop the hemoraging.

In December 1993 Banc One held presentations in New York, Boston, and San Francisco to clarify its position on the use of financial instruments known as derivatives. Banc One used Interest Rate Swaps, the most common type of derivative instrument, to manage interest rate sensitivity. At these presentations, Richard Lodge, the chief investment officer, made clear that Banc One was not a dealer but an end-user of swaps. Lodge emphasized that the bank’s position was one of hedging and not of speculating. They first started using swaps in 1983, and subsequently, when the tax reform act of 1986 eliminated the advantages of municipal bonds as a tool for managing interest rate exposure, their dependence on swaps further increased. By 1993 the notional value of Banc One’s derivative portfolio had grown to $38 billion, a sum almost equal to half its assets! The amounts of Banc One’s swaps contracts depended on various factors such as: the loan demand, the slope of the yield curve, the amount of capital held by the bank, and the cost of cash market versus the derivative market.

Interest rate swaps have several inherent advantages over bonds and other instruments: capital is preserved, liquidity is increased, swaps contracts enabled faster response to changes in market conditions, and swaps can be customized for duration and other variables. In the light of these overwhelmingly positive features of swaps and other similar instruments, Banc One was in the derivative market to stay. Hence, their task was to ease investors fears of these relatively new instruments and reassure them of the prudence of the continued use of these instruments. Banc One intended to be as transparent as possible in reporting its derivative dealings. In the rest of this study we examine the various issues involved in this complex case.

USE OF SWAPS

Like most regional banks, Banc one's natural balance sheet position is asset sensitive, hence interest rates on their assets reset more quickly than on their liabilities. On one hand 73% of Banc One’s assets are indexed to the prime rate, and thus vary with the market, while on the other hand, 50 to 60% of bank liabilities, mostly non-commercial loans (Certificates of Deposit) are fixed rate. This situation is exacerbated by the fact that commercial customers are more responsive to interest rate movements and will exercise their options to refinance quicker, unlike non-commercial customers who are mostly CDs holders which are considered "sticky-fixed." The result of this asset sensitive position is that Banc One’s earnings rise and fall with interest rates. To minimize this interest rate exposure banks traditionally invested in short and medium-term U.S. Treasures and high quality municipal bonds as a hedge against their asset sensitive position. They would borrow at a floating rate and use the proceeds to buy U.S. treasuries and municipal bonds and thus increase their fixed rate assets. The result is a reduction in its asset sensitivity. Prior to 1986 municipal bonds had an added attraction in that banks could deduct 80% of the interest expense incurred on the money which funded their purchase. Furthermore, the income earned on the bonds was tax exempt. The result was that Banc One earned a large spread on the municipal bond hedge. The 1986 Tax Reform Act eliminated the tax deductibility feature of municipal bonds.

Banc One looked for a substitute hedge that would provide high yield and safety. Mortgage backed securities (MBSs) seemed to foot the bill. However, mortgage backed pools provided lower after-tax return and carried a prepayment risk. Because the mortgagor has the option to prepay a mortgage, the holder of the MBSs are short interest rate volatility. This short position is particularly relevant when interest rates fall and mortgagors refinance mortgages en-mass. This is a double whammy for MBS holders since they become awash in cash when interest rates are low and have to re-invest this cash in an unfavorable environment. In addition, when interest rates rise MBS holders are stuck with a below market yield since now the mortgagors have a good deal and they hold on to their mortgages.

To avoid the risks associated with MBS, Banc One held collatteralized mortgage obligations (CMOs). CMOs are pooled mortgage securities. The pool is divided into different groups or tranches which differ in priority of prepayment. The groupings allowed Banc One the ability to better gauge the speed of prepayment. But the prepayment risk still remained. By holding CMOs Banc One had sold a call option on interest volatility. Banc One was short volatility. Thus, the sale of the option increased the banks revenue though at the same time increased its exposure to interest rate volatility. Another disadvantage of CMOs was that they were less liquid than Treasuries or municipal bonds. However, the biggest drawback of CMOs was that the capital adequacy guide lines required that Banc One hold 50% of the principal value of the asset. Cash and Treasures required no risk adjusted weighting while municipal bonds required 20% and municipal revenue bonds required 50% weighting.

In the late 1980’s Banc One realized that it could use swaps to adjust its floating to fixed position. The swap contract acted as a synthetic investment and held numerous advantages over Banc One's prior risk management strategy. First, swaps improved Banc One's liquidity. They also freed up capital for short term investment which provided cash when needed to repay liabilities such as CD withdraws. Second, the off-balance sheet accounting of swaps increased ROA and ROE. The receive fix rate swaps did not appear as an asset or a liability, but were disclosed in footnotes to the financial statements. Yet gains and losses would still be placed on the income statement. If the bank were to use a traditional hedge, buying a fixed rate bond and selling a floating rate security both would appear on the balance sheet: the net result being to lower traditional profitability measures. Finally, as outlined above capital adequacy requirements are a concern to all banks including Banc One. Swaps allowed Banc One to get around these requirements.

HEDGING RISK vs MANAGING RISK

With the success of its initial CMO and swap strategy, Banc One looked to replace these instruments with synthetic CMOs. This lead to the development of Amortized Interest Rate Swaps (AIRS). These swaps allowed for high yields in exchange for taking on prepayment risk. One of the major benefits of AIRs was the substantial reduction of capital adequacy requirements. This reduced capital requirement was cited by Banc one as one of the primary reasons for entering into AIRS. Richard Lodge was quoted by the Wall Street Journal as saying, "Why in the world more banks do not use interest rate swaps to preserve capital, I don't know...It's not an esoteric phenomenon anymore," WSJ February 1993. The AIRS also avoided unpredictable or idiosyncratic prepayment risk associated with MBS and CMOs. In addition the AIRS also were more liquid than traditional CMOs, an important consideration for a bank that might need or want to re-hedge its position.

How do AIRS work? The AIRS replicated the mortgage backed securities with similar prepayment features. The notional amount of the AIRS were reduced or amortized if interest rates fell. As interest rates declined, the AIRS would amortize faster. Just like CMOs, Banc One would have to reinvest just when market yields were at their lowest. If market rates rose the instrument’s maturity would wind up longer than expected, again leaving Banc One with below market returns.

What are the advantages of AIRS? When Banc One entered into the contract it received a fixed 120 bases points over the current Treasury security of the same maturity. By contrast, a comparable CMO would yield 100 basis points over treasury and a plain vanilla swap only 20 basis points over Treasury. Thus Banc One "goosed up" its returns by entering into the AIRS. In effect Banc One was willing to sell a call option on interest rate volatility in order to earn above market returns. The premium it received for selling this embedded call option was part of the 120 basis points it received. Thus Banc One was short a call option on interest rate volatility. The value of the call Banc One sold increased with interest rate volatility.

Mortgage backed securities like CMOs, are tied to the high end of the yield curve because mortgages are long term obligations. The high end of the yield curve is less volatile than the short end of the curve. But the AIRS with quarterly payment periods are tied to the more volatile short end of the yield curve. The 20 additional basis points Banc One received on AIRS over traditional CMOs reflected the additional interest rate volatility sensitivity built into AIRS.

The "prepayment risk" or amortization feature of AIRS complicated the task of measuring interest rate risk. The embedded option made Banc One's earnings sensitivity nonlinear: Banc One's returns now followed a convex path. This convexity or nonlinear risk profile because of the embedded options introduced a second order exposure to Banc One's position. This second order derivative in effect exposed the bank to gamma sensitivity in addition to the delta sensitivity of interest rates. The bank now had significantly greater exposure to the volatility of interest rates. This volatility exposure was much greater than if the bank used plain vanilla swaps or Treasury securities to hedge their risks. The effectiveness of AIRS as hedging substitutes for Treasuries and CMOs depended critically on the cash flow characteristics of Banc One's on balance sheet assets and liabilities. Banc One chose to trade the risk of increased exposure to volatility for higher earnings. This strategy would pay off for the bank if stable interest rates prevailed. When interest rates suddenly moved upwards in late 1993 and early 1994 Banc One's interest rate volatility exposure hurt them by negatively effecting the AIRS.

The question we must now ask is: Was Dick Lodge totally candid in his 1993 presentations? At the time he went on record as stating that Banc One used swaps only to hedge risk and not to speculate. Although Banc One certainly did use AIRs and other derivatives to hedge interest rate exposure, the above analysis reveals that in doing so Banc One took on exposure to interest rate volatility. Our feeling is that it would be naïve to assume that Banc One did not know what it was doing. By trading volatility risks for higher returns the bank was taking a position on volatility. Labeling this as speculation may be somewhat of a strong statement, but there is no doubt that Banc One took a view and acted on it. We feel that Mr. Lodge must be more definitive in his explanation of Banc One’s derivative usage.

MANAGING SWAP RISKS: BASIS RISK, COUNTER PARTY RISK

Although swaps are superior to cash instruments in managing interest rate sensitivity, the use of swaps raised additional issues. Unlike Treasuries, or bonds, swap derivatives brought on basis risk and credit risk which Banc One had to deal with. The floating leg of most conventional swaps are indexed to LIBOR which changes daily. However, Banc One's floating rate assets were mostly based on the U.S. prime rate which changed infrequently. The difference in the spread of these two indices caused a basis risk problem. To manage the bases risk Banc One entered into additional "bases swaps." The bases swaps required Banc One to pay floating rate based on prime and receive floating rate based on LIBOR. This simple transaction allowed Banc One to confidently deal with the bases risk brought on by the original swap contract.

The second issue confronting Banc One was credit risk. U.S. Treasuries posed no credit risk and municipal bonds posed only minor credit risk. Swaps, however, exposed Banc One to the risk of counter party default. Swaps naturally mitigated this credit risk in two ways. First, the higher yield as compared to treasuries compensated for the additional credit risk. Second, while the entire principal of a bond or security is at risk, with a swap only the net payment, not the notional amount is at risk.

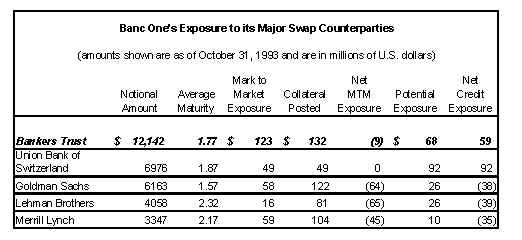

Banc One went beyond these provisions by establishing strict policies for managing its counter party exposure. First, the counter parties it dealt with were rated no lower than single A. Second, Bank One constantly monitored its mark-to-market exposure to each counter party. Total derivative and direct lending exposure to any one counter party was limited by in-house guide lines. Finally, Banc One required that each counter party post collateral in the form of securities or cash against the credit exposure. The amount of collateral posted was equal to Banc One's possible losses in one month from an extreme movement in interest rates. In addition, counter parties were required to post additional collateral as the market value of the swap changed over the life of the contract. The net result was that Banc One was not exposed to sums due for which it was not fully collateralized. If a counter party was to default, the mark-to-market value of the collateral would allow Banc One to enter into a new swap with a new counter party to replace the defaulted agreement. These collateral agreements were unique. Banc One's solid credit rating allowed it to obtain these collateral agreements. Furthermore, Banc One disclosed the identity, notional amount, amount of collateral, potential exposure, and net credit exposure of each counter party. A list of the counter-parties with whom Banc One had swap agreements in October 1993 is shown below.

STOCK PRICE

Banc One’s stock price dropped dramatically during the latter half of 1993 from $44.36 to a year end close of $35.57, nearly a 20% drop. There are many theories to explain why the stock price dropped and why shareholder wealth suffered. We will attempt to explain the theories we subscribe to. First, Banc One was focused primarily on earnings volatility risk and had a strategy of entering into swaps which would enabled them to dampen their susceptibility to asset interest rate sensitivity. Based on their analysis, Banc One determined that an interest rate fluctuation of more than + 100 basis points was unlikely. Given this assumption, the decision was made to enter into AIRS to take advantage of higher yields for such low interest rate volatility. This strategy theoretically allowed Banc One to gain an additional 100 basis point advantage over Plain Vanilla Swaps (PVS). This swap strategy essentially guaranteed them constant positive earnings over the next ten years in the range of + 100 basis points. By effectively locking in earnings over this very small range, Banc one exposed itself to large volatility risk.

Based on their analysis, the firm predicted that low volatility in interest rates would not have an effect on shareholder value. But, because stock value is the sum of all expected future cash flows discounted back at the current discount rate, its value is effected by changes in the discount rate. As interest rates increased by 175 basis points between November ‘93 and October ‘94, Banc One’s earnings decreased drastically. This reduction adversely effected the stock value. Intuition tells us that if the cash flows decrease over time and the discount rate continues to increase, the value of the stock will decrease. If we look at the mathematical implications, the formula shows us that decreased earnings means the numerator is becomes smaller while the increase in ‘r’ forces the denominator to become larger. The ultimate result is the stock price decreases.

Second, the fact is that in 1993 the business world was still trying to sort out the issues associated with using derivatives, especially exotic swaps, to decrease interest rate risk. The industry was comfortable with the use of CMOs and plain vanilla swaps as risk management tools. The use of AIRS was viewed as speculative in nature and was not completely understood by many analysts and investors. Banc One’s derivative portfolio consisted of numerous AIRS and generated a large portion of the firm’s income (around 26%: $442 million out of $1.7 billion). Although Banc One tried to formulate an extensive teaching and disclosure plan, the level of acceptance and understanding was not adequate to maintain stock value. Unfortunately, after the disclosure meetings many of the analysts and investors were left with more questions than before. This resulted in analysts and investors making subjective assessments of the firm’s future cash flows as being "risky." Their assessment carried with it a risk premium, which in effect put downward pressure on stock prices. Again, intuition tells us that if the expected cash flows are risky the discount rate rises: the stock price and shareholder value will decrease. Mathematically, the denominator is increasing causing the stock price to decrease.

Finally, the market was extremely leery of the use of exotic derivatives such as AIRS as risk management tools because of the events in Orange County, California, and cases involving Banker’s Trust at the time. The disaster that befell them and the apparent risks associated with the extensive use of derivatives only served to discount the positive aspects of Banc One’s strategy. Furthermore, the disclosure that Bankers Trust was Banc One’s largest counterparty (see chart on page 11) did not help quell investors fears. The market fears forced the analysts to subjectively add a risk premium, which caused downward pressure on the firm’s stock prices. As with the point above, intuition tells us that if the expected cash flows are smaller while the discount rate is rising, the stock price will decrease.

INTEREST RATE VOLATILITY AND EARNINGS

As we saw above, Banc One did not disclose that they had actually increased their exposure to volatility in order to earn higher yields while hedged against small movements in interest rates. During the same ten year time period, prior to 1993, Banc One had also swapped into a position to keep a relatively stable stream of earnings for the next ten years of 2.37%. How do these two issues relate to each other and how did they adversely affect the stock and firm values?

First, the issue of volatility risk is significant to Banc One because they essentially counted on interest rate movements being very small over the life of their swap agreements. They demonstrated this by entering into numerous AIR swaps, which hedged out almost all risks associated with small interest rate movements while exposing them to large volatility risk. There are two reasons why this may have happened: improper analysis of possible future interest rate fluctuations or a deliberate assumption of volatility risk in return for higher yields.

Second, is volatility in earnings of significant risk to Banc One? The firm had adequately hedged against variability in earnings by essentially swapping into a situation where they were receiving a higher overall interest rate than they were paying out. By doing this, they locked in a "fixed spread" and stabilized their earnings. The stabilization of earnings through the year 2004 effectively resulted in a no growth earnings situation. Again, although the firm was hedged against small changes in interest rates, a large swing in interest rates would drive down earnings and force the discount rate at which future cash flows are discounted to rise, lowering the value of the stock. With the firm hedging against their exposure to changes in earnings over such a small range in interest rates, they have inadvertently exposed themselves to another increased risk in volatility. It is evident to us, that the exposure to volatility risk was the key ingredient to the devaluation of Banc One’s stock prices. The need for minimized volatility in earnings is clearly essential. There must be an appropriate balance between the value of the spread gained by investing in AIRS and the amount of exposure a firm faces in terms of interest rate volatility.

DISCLOSURE

Banc One realized early on that their derivative usage was being characterized as speculative in nature and that many of its investors were simply unclear on the use of derivatives as a hedging tool. Under these circumstances, the Chairman and CEO of Banc One, John B. McCoy, embarked on a plan to make full disclosure of Banc One’s off balance sheet derivatives portfolio activity. This discussion will focus primarily on the disclosure associated with one particular derivative, the interest rate swap. During the ten years prior to 1993, Banc One had made a significant move away from the use of United States Treasury securities to manage interest rate sensitivity and instead dealt with interest rate risk by careful selection of interest rate swapping arrangements. By the end of 1993, Banc One held an off balance sheet derivatives portfolio of notional value of approximately $38 billion which amounted to a sum nearly half that of the assets on its balance sheet.

How important is a strategy of disclosure to Banc One? First, one must analyze the "pros and cons." The most important advantage in McCoy’s opinion, was that disclosure was the only way to educate the public in the area of derivatives usage. Knowledge was the key to the market’s positive assessment of Banc One’s strategy. Further, a positive assessment of their strategy was essential to the value of the firm’s stock. Full disclosure of off-balance sheet activities was not required by the FASB and was certainly not a common practice among the other banks utilizing derivatives. What are the cons associated with disclosure of financial activities not required? One important disadvantage is that disclosure can signal other firms in the industry as to your competitive strategy. It may also dispel other firm’s fears of your ability to conduct business in a price warfare environment and actually force competitors to engage in such practices.

Given that the pros far outweigh the cons in this case (and for the sake of our argument), why were McCoy’s efforts to disclose the firm’s derivatives package and its portfolio management strategy in late 1993 and early 1994, largely unsuccessful? It is our opinion that in the hopes of educating investors and analysts, McCoy and Lodge actually confused them about Banc One’s overall derivatives strategy. We hold McCoy and his financial staff accountable for several reasons. The most important reason is that in disclosing the off balance sheet figures, they did not adequately represent the risk position of the firm after the hedge was set in place. Our analysis follows: Because Banc One relied heavily on Amortizing Index swaps (AIRs), it put itself in an excellent position to manage interest rate sensitivity between the ranges of + 100 basis points. This very important decrease in exposure to small interest movements was only one half of the story and was highlighted in their derivatives presentations in New York, Boston, and San Francisco. However, the firm neglected to highlight the significant increase in exposure to interest rate movements above and below 100 basis points. Consequently, some investors and analysts were able to foresee the shift in convexity in the value function of Banc One with the heavy use of AIR swaps, and the omission of this information further added to their skepticism. The failure to address this issue had the effect of painting a picture that was "to good to be true." Discounting investors’ knowledge/ignorance of all the specifics involved in derivative risk management techniques, the natural reaction of risk conscious investors is to question the "perfect" investment’s merit and perhaps even to put a subjective negative twist on the firm’s future cash flows and ultimate value. This inadequate disclosure contributed to the decline in the firm’s stock price.

RECCOMMENDATION

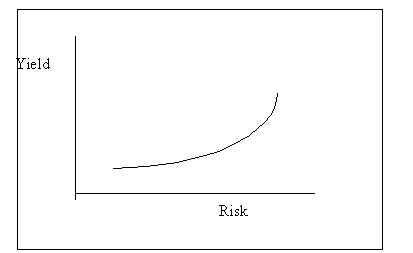

A basic tenet of finance is that in equilibrium the rate of return the market expects on an investment increases as the risk involved in the investment increases. A stylized representation of this is shown in the figure below. Thus, a corporation that assumes a risky strategy should anticipate the market to demand a correspondingly high return for its investment.

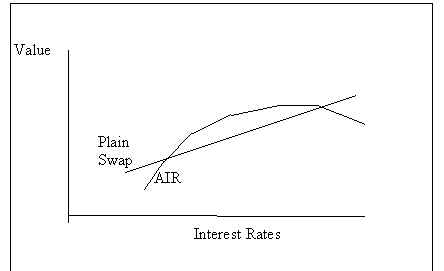

We saw that a sizable portion of Banc One's fixed rate investments were in mortgage backed securities, CMOs, and AIRs. These three instruments all involve prepayment risk (in addition some of the bank’s liabilities, like CDs, also involved prepayment risk). The diagram below shows the value of an AIR contract, which is really a synthetic CMO, with respect to a plain vanilla swap as a function of interest rates.

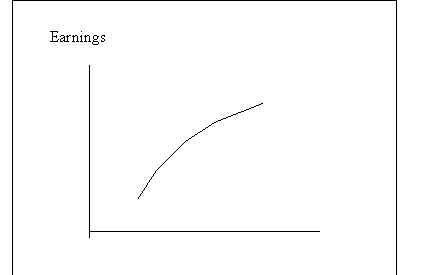

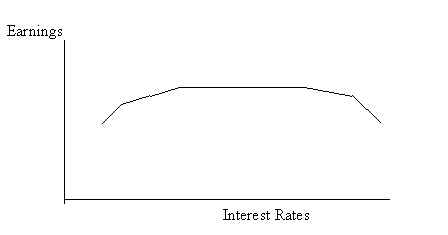

Notice that, for a range of interest rates AIRs pay better than plain vanilla swaps but outside this range the value of AIRs drops below that of a plain swap. Hence, because of the three fixed income instruments: mortgages, CMOs, and AIRs, which have similar yield curves, the earnings for Banc One corporation assumes convexity with respect to interest rate fluctuations as shown in the diagram below. When this position is hedged

using plain vanilla swaps the earning curve for Banc One is as shown below. As can be seen in the diagram below, for a range of interest rates Banc One’s earnings are high but if the rates were to fluctuate outside this range its earnings would drop dramatically. Banc One took this position hoping that interest rates would not fluctuate beyond this range. It took this risk in its pursuit of higher yields and "lost its bet" since interest rates rose higher than it had anticipated in late 1993 and early 1994.

Banc One should realize that the market is efficient and the fall in their stock price was in part due to the volatility created in its earnings because of its large fixed rate portfolio of AIRs, CMOs, and mortgages which are exposed to volatility risks. Hence our recommendation to Banc One is the following:

BIBLIOGRAPHY

Banc One Corporation (A): Harvard Business School Case, Dale O. Coxe, June 1995.

Banc One Corporation: Asset and Liability Management. Harvard Business School Report, Ben Esty, Peter Tufano, and Jonathan Headley.

Derivative use in Banks: The six ironies, Robert Albertson, Goldman Sachs & Co., Journal of Applied Corporate Finance, Vol 7, No. 3, p. 52, Fall 1994.

The Use of Index Amortizing Swaps by Banc One, Christopher James and Clifford Smith, Journal of Applied Corporate Finance, Vol 7, No. 3, p. 54, Fall 1994.

Comments on Banc One, Ethan Heisler, Salomon Brothers, Journal of Applied Corporate Finance, Vol 7, No. 3, p. 59, Fall 1994.

What Can Bankers Learn About Hedging Strategy From The Banc One Case, Edward J. Kane, Journal of Applied Corporate Finance, Vol 7, No. 3, p. 61, Fall 1994.